Click Play to listen to our generated podcast. Access our full podcast library here.

PepsiCo recently announced a partnership with the National Geographic Society that supports scientists, agronomists, and farmers to work on soil health measurement, biodiversity tracking, and data-driven farming tools, including the use of satellite monitoring and artificial intelligence to translate soil science into field-level decisions. The significance isn’t just the funding. It’s the shift in posture.

Rather than waiting for consumers to reward niche regenerative brands at the checkout line, one of the largest food companies in the world is investing upstream, directly in how corn, oats, potatoes, and other foundational crops are grown.

For years, regenerative agriculture has lived in two places: academic soil science and marketing language. It has been praised as the future of farming and criticized as too loosely defined to scale. Now corporate dollars are being tied to measurement frameworks and farmer transition models. The question is not whether regenerative agriculture sounds promising. The question is whether this moment represents structural change in how American farmland is managed?

How We Got Here

Modern American agriculture did not emerge accidentally. After World War II, farm policy prioritized yield, efficiency, mechanization, and shelf stability. Commodity crops such as corn, soybeans, wheat, and cotton became the backbone of a system designed to feed a growing population affordably and reliably. Technological innovation accelerated productivity. Food became cheaper relative to income. Caloric abundance was no longer the national crisis it once had been.

But efficiency brought tradeoffs. Decades of intensive production in some regions reduced soil organic matter and simplified crop rotations. Erosion and nutrient runoff became persistent environmental concerns. (Think of the Dust Bowl). Farmers grew extraordinarily good at producing high yields, but questions began to surface about what was happening with the integrity of the soil and the watersheds beneath the farmland.

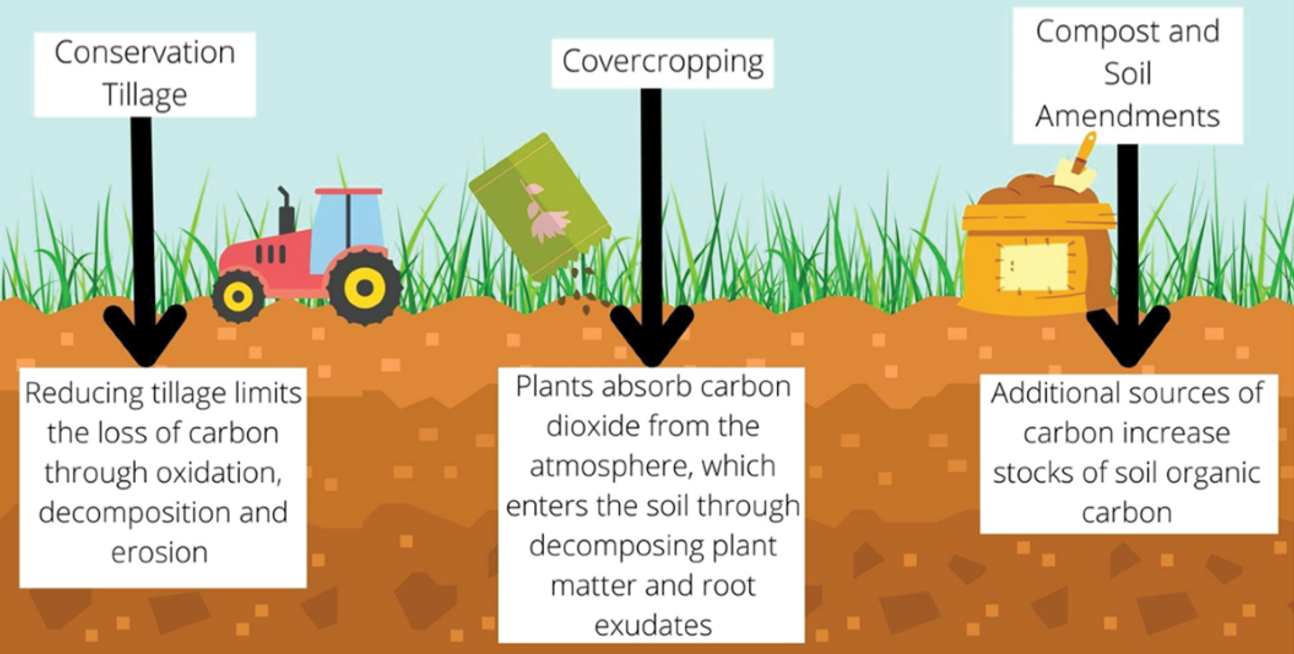

Regenerative agriculture emerged as a response to those concerns. Rather than focusing solely on sustaining current productivity levels, regenerative advocates argued for rebuilding soil health. Practices typically associated with regenerative systems include minimizing soil disturbance, keeping the ground covered with living roots, diversifying crop rotations, spraying bacteria healthy for soils, and in some cases integrating livestock. The promise is compelling: healthier soils can hold more water, resist erosion, improve biodiversity, and store carbon.

For years, however, regenerative agriculture remained aspirational. It was discussed at conferences, featured in documentaries, and highlighted in brand campaigns.

But scaling and measuring it across millions of acres of commodity farmland proved more complicated.

The Definition Problem

One of the biggest obstacles has been definition. Unlike organic agriculture, which is governed by federally regulated standards and certification protocols, regenerative agriculture has no single nationally accepted framework. One company may define it as reducing tillage. Another may require cover crops. A third may include carbon measurement, livestock integration, or biodiversity targets.

This variability has drawn legitimate criticism.

To make it more complicated, each farm has its own unique weather pattern, soil diversity, and water quantity. Growing potatoes in Idaho requires a different level of regenerative agriculture than growing potatoes in Pennsylvania.

Scientists have questioned how soil carbon gains are measured and whether they persist over decades. Economists have debated whether regenerative systems can maintain yields at scale. Policy analysts have noted that practices successful in one climate zone may not translate seamlessly to another. Without common metrics, regenerative agriculture risked becoming a flexible marketing term, another ‘sustainable’ phrase, appealing but difficult to evaluate. That is where the current shift becomes important!

When Procurement Drives Change

Large consumer packaged goods companies like Pepsi, occupy a powerful position in the food system. They purchase enormous quantities of agricultural commodities each year, from corn and oats to potatoes and sugar. Their procurement decisions influence planting choices across vast regions.

Historically, those procurement contracts rewarded uniformity, yield, and efficiency. They shape monoculture systems and optimize supply chains for cost and predictability. If those same contracts begin rewarding soil health outcomes, the incentives across millions of acres begin to change. A change that consumers have been demanding.

It is difficult to alter the behavior of millions of individual consumers.

It is comparatively straightforward to alter procurement standards among a handful of multinational buyers whose contracts reach deep into rural America.

When corporate purchasing criteria shift, farming practices often follow. This is why corporate involvement in regenerative agriculture matters. It moves the conversation from niche brands and boutique labels, direct from the farm, and majority consumer-influenced, to instead massive mainstream supply chains.

Measurement Changes the Equation

Perhaps the most consequential shift in this new phase of regenerative agriculture is not the rhetoric surrounding it, but the infrastructure developing beneath it. For years, regenerative commitments were largely descriptive. Companies spoke about improving soil health or supporting farmers without clearly defining how progress would be verified. That is beginning to change.

PepsiCo is not alone in moving toward measurable systems.

- General Mills has committed to advancing regenerative agriculture across one million acres by 2030, working with academic researchers and retail partners such as Walmart to quantify soil carbon, biodiversity, and farmer outcomes within its wheat and dairy supply chains.

- Nestlé has launched pilot programs across key sourcing regions that tie financial incentives and agronomic support to documented soil improvements.

- Unilever has embedded regenerative agriculture into its climate transition planning, emphasizing traceability and supplier-level verification across tea, soy, and vegetable oil systems.

- Cargill, one of the world’s largest agricultural commodity traders, has expanded its RegenConnect program to reward farmers for measurable outcomes, linking soil-health practices to carbon markets and corporate buyers seeking verified supply chain improvements.

Retailers, too, are recognizing that long-term supply chain resilience depends on what happens at the field level. What distinguishes this wave of investment from earlier sustainability pledges is the insistence on verification. Regenerative agriculture is increasingly being pulled into systems that demand proof.

Advances in satellite imagery now allow companies to confirm whether cover crops are planted and crop rotations diversified. Soil sampling protocols are becoming more standardized, enabling year-over-year tracking of organic matter. Digital agronomic platforms use artificial intelligence to model nutrient flows and water retention patterns.

At the same time, sustainability reporting frameworks require companies to account for Scope 3 emissions, the indirect emissions embedded in agricultural supply chains, drawing soil practices directly into formal climate disclosures.

In other words, regenerative agriculture is (finally) being translated into data.

When soil organic matter is tracked over time, when water infiltration rates are measured, and when carbon metrics are tied to financial filings, regenerative practices shift from philosophy to performance indicator. Data opens the door to sustainability-linked loans, carbon markets, and supply contracts tied to environmental outcomes. It also invites scrutiny, which may ultimately strengthen credibility.

Measurement does not eliminate uncertainty. Soil systems remain complex, shaped by weather variability, crop type, and regional conditions. But measurement narrows subjectivity. It reduces the distance between marketing claim and field-level reality, and that narrowing may be what allows regenerative agriculture to scale beyond aspiration.

The Farmer Perspective

For farmers, transitioning practices is not simply an environmental decision; it is an economic one. Margins in commodity agriculture are often tight, and even modest yield variability can have financial consequences. Cover crops require seed costs and management time. Reduced tillage may require new equipment or altered weed management strategies. Integrating livestock into crop systems demands infrastructure many grain farmers no longer have.

Without financial support, experimentation carries risk. “Historically, when we’ve transitioned farms, we’ve just eaten those losses annually,” says Matt Fitzgerald of Fitzgerald Organics in Minnesota, describing the financial strain of cover crop and regenerative transition before securing multi-year financing support. “Getting funding to transition to regenerative practices can be a challenge for farms of all sizes, but it’s a necessity if we want to have abundant harvests for generations to come.”

Corporate regenerative programs often attempt to address this through multi-year contracts, cost-sharing arrangements, or technical assistance partnerships. By offsetting early transition expenses and offering longer-term purchasing stability, companies reduce the financial uncertainty farmers face.

Still, adoption will not look identical across all farm sizes or regions. Large operations may integrate practices differently than smaller diversified farms. Climate variability adds another layer of complexity. The transition to regenerative systems is gradual and context-dependent, not instantaneous.

What This Means for American Farmland

If regenerative practices scale meaningfully, the long-term implications for farmland could be substantial. Soils with higher organic matter content typically retain water more effectively, which can reduce vulnerability during drought conditions. Improved soil structure may decrease erosion and runoff. Reduced reliance on certain inputs could alter cost structures over time.

However, regenerative adoption does not guarantee uniform outcomes. Yield impacts vary by crop and region. Carbon sequestration rates depend on climate, soil type, and management consistency. Policymakers and researchers continue to debate how best to quantify long-term soil carbon permanence.

What appears increasingly clear is that farmland management is entering a data-intensive era. Soil is no longer merely a substrate for crop production; it is becoming an asset class evaluated for resilience and climate performance.

The Consumer Role Going Forward

For you, as our reader, the implications may be subtle but meaningful. Instead of relying solely on niche regenerative brands, mainstream packaged foods could increasingly incorporate ingredients sourced from farms using soil-health-focused practices. Sustainability becomes embedded upstream rather than displayed exclusively on boutique labels.

This shift may not dramatically change grocery store aesthetics overnight. But it suggests a movement from consumer-driven pressure toward supply-chain-driven reform.

Consumers will still influence demand. Yet the mass of change may expand beyond the checkout line to the contract negotiation table.

For years, regenerative agriculture hovered between idealism and ambiguity. It promised healthier soils and more resilient ecosystems but struggled with definitional clarity and scalable infrastructure. If major food companies continue tying financial incentives to measurable soil outcomes, regenerative agriculture may move from aspiration to operational standard. Data, not just narrative, will determine its credibility.

Whether this moment represents genuine transformation or an incremental evolution remains to be seen. Agriculture has always adapted slowly, shaped by weather, economics, and policy. But when procurement contracts begin valuing soil health alongside yield, the system’s incentives shift.

Regenerative agriculture may not be a silver bullet. It may not reverse decades of soil degradation overnight. Yet the convergence of corporate capital, scientific measurement, and farmer partnership suggests that something more structural than a marketing trend is unfolding.