Click Play to listen to our generated podcast. Click on links for transcript and our full podcast library.

In 2016, we wrote about the excitement consumers and investors had for a new type of protein. By 2013, investors enthusiastically poured $3 billion into this new technology hoping for traction with consumers and lower production costs. This led many of us to assume we would be eating burgers, fish and chicken grown in bioreactors by 2025. But that has not materialized.

While some companies are making slow progress, the technology is not leaping forward as planned due to consumer perception, state regulatory blockades, and cost of production compared to regular meat.

A large impediment is the regulatory dichotomy between the U.S. government and individual states. While the FDA and the USDA have approved cultivated meat from UPSIDE Foods, some states have banned cultured meat for human consumption.

First, let’s ask: “Is it safe to eat?”

Learning how cultivated meat is made is the first step in understanding this process.

A biopsy is taken from an animal or bird. These cells are put in bioreactors, along with nutrients to help them grow. The ‘vitamins’ used to proliferate the cells consist of amino acids, glucose, vitamins, inorganic salts, along with protein growth factors. This recipe is very similar to what is produced by an animal’s metabolism to make them grow.

A biopsy is taken from an animal or bird. These cells are put in bioreactors, along with nutrients to help them grow. The ‘vitamins’ used to proliferate the cells consist of amino acids, glucose, vitamins, inorganic salts, along with protein growth factors. This recipe is very similar to what is produced by an animal’s metabolism to make them grow.

The objective is to have the same, or better, nutritional value as cattle, chickens, pork or fish. After the cells have grown into muscle fibers, they are considered meat… just like the kind from a cow or chicken.

The FDA and the USDA worked closely with various cultivated meat companies to ensure that the processes used to produce meat are safe and lawful under the Federal Food, Drug and Cosmetic Act. They have also held public meetings to ‘better understand the science of animal cell culture technology, discuss potential hazards and labeling considerations, and to listen to consumer concerns.”

Upside Foods was the first for federal approval with their chicken products. Focusing on cultivated chicken, they are one of the most well-funded and recognizable companies in the sector. They built one of the first U.S. large-scale cultivated meat facilities and are focused on regulatory pathways and premium chicken products, as well as beef and duck.

“We make the chicken chickens dream about! Our cultivated meat is grown in a controlled environment with no need to raise and slaughter billions of animals.”

– Upside Foods

Some advocates argue that cultivated meat may be considered safer and more sustainable — a selling point for health and environmentally-conscious consumers concerned about hormones, antibiotics, and effects on the earth.

But social media can cloud the landscape among consumers, too, with claims like “cultivated meat causes ‘Turbo Cancer’ because the cells are immortal.” Statements like this are false. To make cultivated meat without constantly running biopsies on animals, scientists use cells that can divide indefinitely. While cancer cells also do this, that’s where the similarity ends.

Furthermore, by the time the meat hits your plate, those cells are dead. And even if they weren’t, your stomach acid destroys them instantly. You cannot catch cancer from eating a cell.

Get ready for your pop quiz! Would you eat cultivated meat?

Continue reading and then answer a few questions at the end.

States banning Cultured Meat

Despite its safety, seven states are banning cultured meat, it seems, to protect their farmers and ranchers who are growing traditional meat.

Today, Florida is fighting back against the global elite’s plan to force the world to eat meat grown in a petri dish or bugs to achieve their authoritarian goals,” said Governor Ron DeSantis. “Our administration will continue to focus on investing in our local farmers and ranchers, and we will save our beef.”

The result is a patchwork of contradictory rules. It is currently legal to serve cultivated chicken in a high-end restaurant in San Francisco but selling that same chicken in Miami could land you with significant fines.

Here is the current breakdown of the “meat map”:

Given that cultured meat is such a small player in the overall protein market today, it seems unlikely that it is about to put cattle ranchers and poultry producers out of business. In discussing this with Uma Valeti, CEO of Upside Foods, he equates this technology to similarities to the energy sector.

“The world needs to meet its energy needs both reliably and sustainably. That is why wind and solar power have been introduced into the energy markets.

This concept is like cultivated meat as part of the global protein market. The difference is that not one state is shutting down wind and solar to protect the energy companies.”

– Uma Valeti, CEO of Upside Foods

He has a point. Well-known energy companies like Chevron, Shell, and BP have embraced wind and solar as part of their energy strategy.

The same applies to the meat industry.

In fact, these companies are some of its biggest supporters and investors.

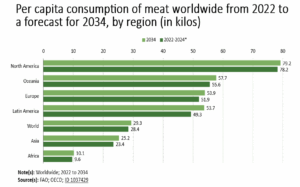

More people mean more protein. By 2034, the global population will grow an extra 600 million people to 8.8 billion, with protein needs projected to grow to 406 million metric tons from 351 million in 2024.

Who are the players?

As of today, there are at least 10 companies that believe the future innovation of meat belongs in the lab.

Whether it is chicken, beef, shrimp, or bluefin tuna, they all look at cultivated meat with an eye toward the planet. The science is proven—we can grow meat in a lab, sustainably.

“Rather than raising whole chickens, pigs, or cows, we grow only the meat we want to eat—directly from real animal cells.

At scale, it will be a more humane and future-friendly way to grow high-quality food for meat lovers everywhere.”

– Upside Foods

Good Meat also focuses on plant, human, and animal well-being, stating that “any choice we make affects families across the globe. Our health and our planet’s health are deeply connected.”

But it is not just the solely-focused companies that are interested in alternative protein. The large beef and chicken companies are, as well.

- Believer Meats, an Israeli cultivated meat company back by Tyson Foods, recently filed for bankruptcy due to funding and operational issues, despite having been close to success with a safety confirmation from the FDA.

- JBS, the world’s largest meat processor, bought a majority stake in a Spanish company, Biotech Foods

- Cargill invested in UPSIDE and is backing Aleph Farms, which is focused on growing complex beef steaks.

Granted, this market is small.

Granted, this market is small.

Cultivated meat is only 0.002% of the global protein market cap. And if we were to look at sales, it is 0.000003%.

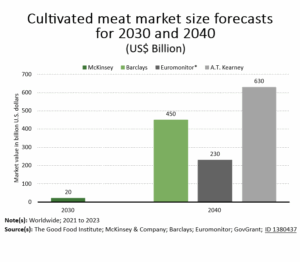

However, research firms find the market ripe for significant growth.

McKinsey projects a positive 2030 forecast for cultivated meat demand, while Barclays, Euromonitor, and A.T. Kearney see a much larger market for these products by 2040.

What does the consumer say?

Here is where it gets interesting.

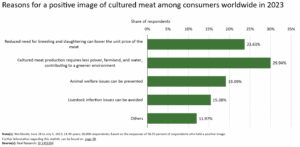

Statista carried out a global survey in 2023 asking consumers whether they were willing to try cultured meat. 62% said yes, 38% said no.

The 62% who were willing to try it have various environmental and animal welfare reasons.

However, Mintel’s report was a little less optimistic.

They noted that consumers were concerned about how cultivated meat fit into their country’s culture, especially in Europe. About 45% of French and Spanish participants were concerned about traditions and culture. The rest were undecided.

The UK was a little more in line with the global survey of Statista where 63% of the younger generations were willing to try it.

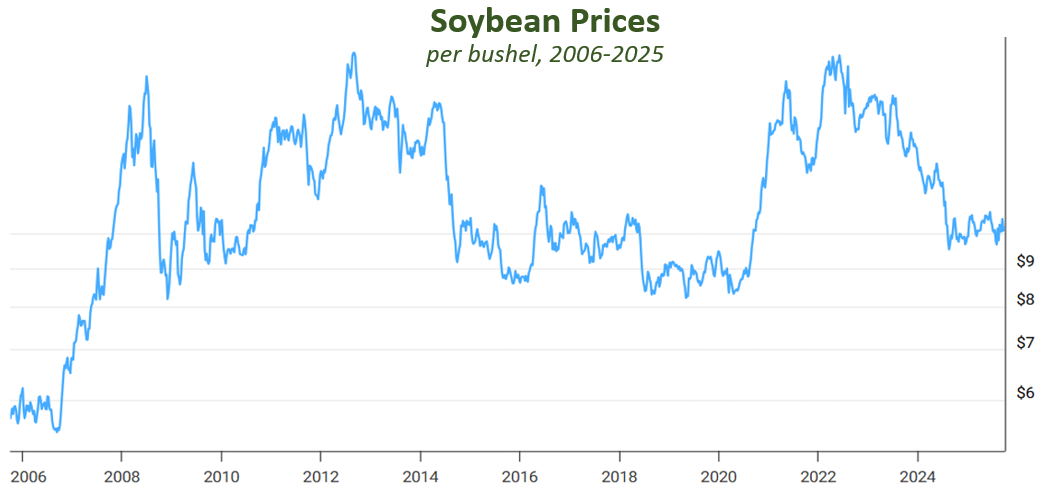

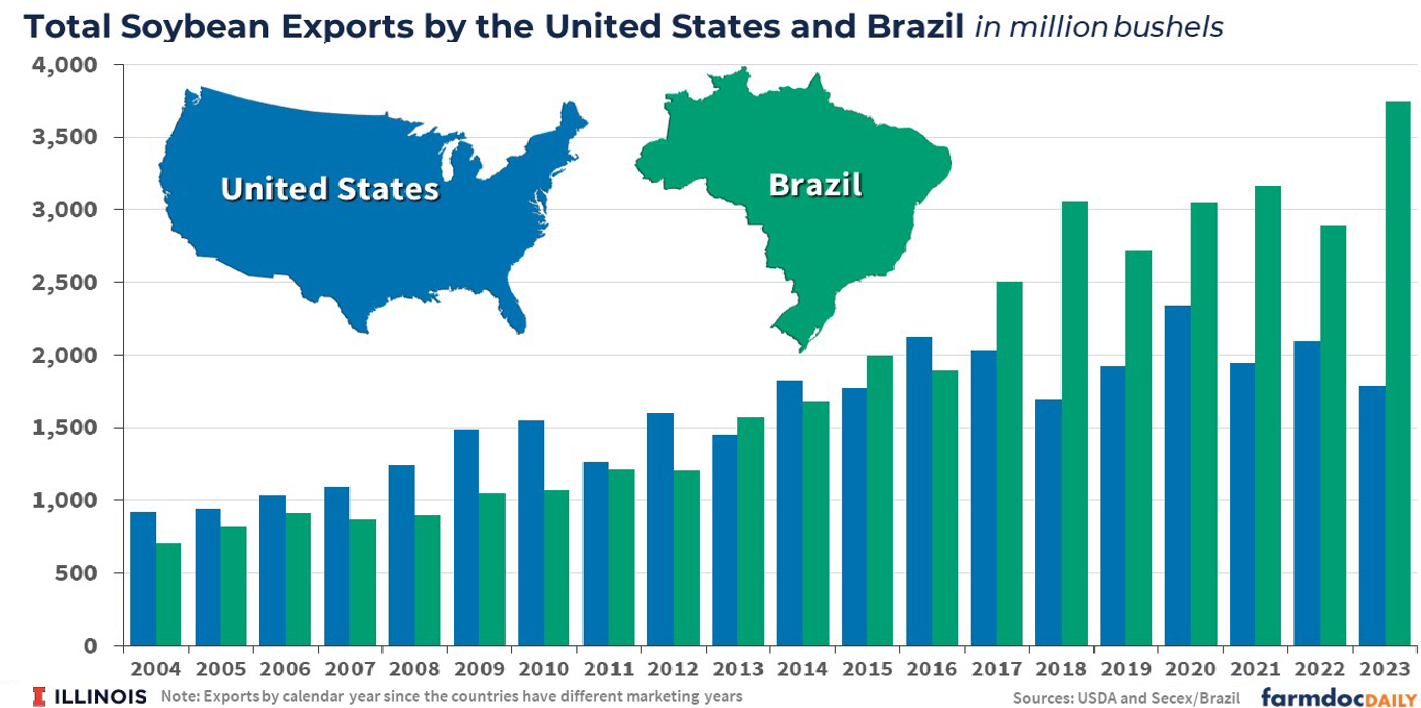

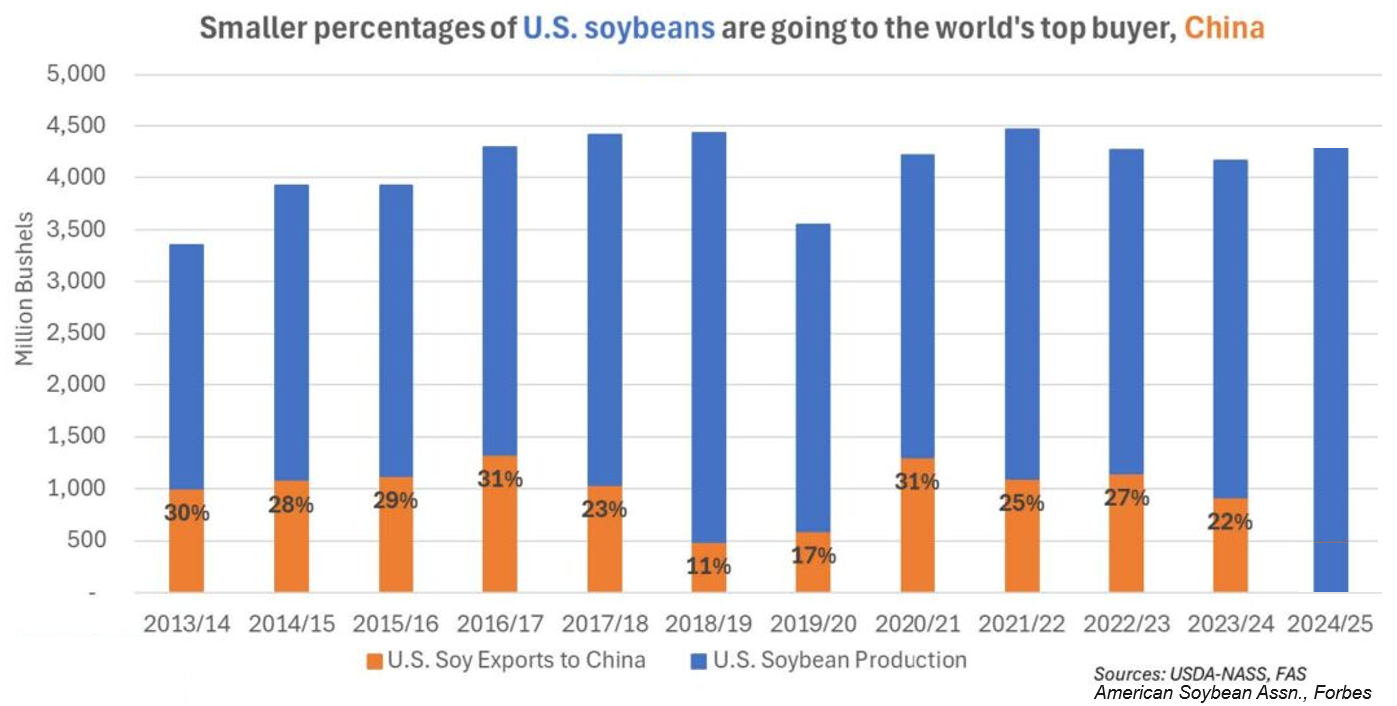

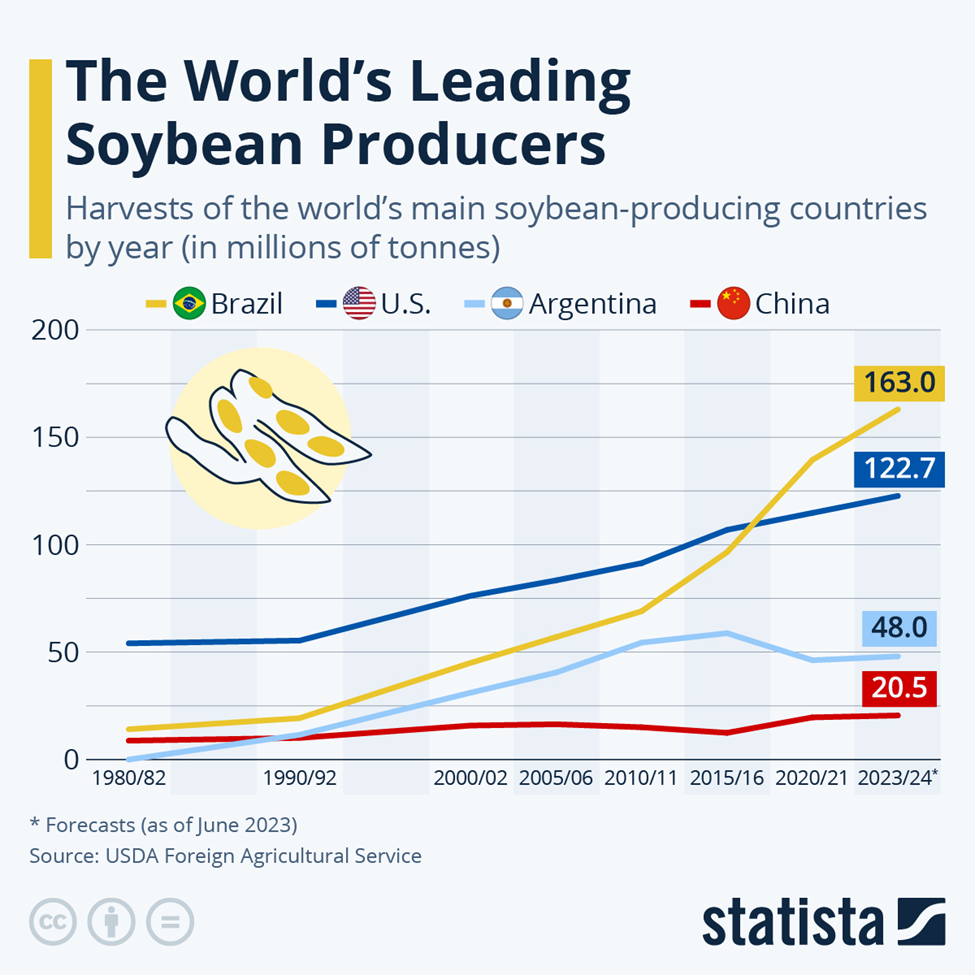

While U.S. soybean growers have had to deal with the adverse effects of the on-going trade dispute with China, Brazilian growers have stepped into the fill that gap.

While U.S. soybean growers have had to deal with the adverse effects of the on-going trade dispute with China, Brazilian growers have stepped into the fill that gap.

General Mills has teamed up with

General Mills has teamed up with

In 2023, over

In 2023, over

The FDA’s decision to act on Red Dye No. 3 after decades of inaction may signal a shift towards more proactive regulation of food additives.

The FDA’s decision to act on Red Dye No. 3 after decades of inaction may signal a shift towards more proactive regulation of food additives. There are many substitutes for Red Dye No. 3, such as beet juice, purple sweet potato extract, red cabbage extract, carmine, and pomegranate juice. These natural substitutes align with growing consumer preferences for clean-label ingredients. After all, many of us would rather consume pomegranate juice in Jell-o than red dye.

There are many substitutes for Red Dye No. 3, such as beet juice, purple sweet potato extract, red cabbage extract, carmine, and pomegranate juice. These natural substitutes align with growing consumer preferences for clean-label ingredients. After all, many of us would rather consume pomegranate juice in Jell-o than red dye.

You wonder: are your children charging too much? So you go back and encourage them to drop their price to $1.00, knowing that at least they should make $25.00 for the day. This will take most of the summer, but an iPhone is still in their future. Life is good.

You wonder: are your children charging too much? So you go back and encourage them to drop their price to $1.00, knowing that at least they should make $25.00 for the day. This will take most of the summer, but an iPhone is still in their future. Life is good.