Food Trends ’26: Higher Standards

The Dirt

This year's food trends reflect the realities of financial pressures, smaller appetites, and information fatigue, while still wanting food to support health, comfort, and functionality. This shift is showing up not only in consumer behavior, but increasingly in how nutrition itself is being discussed at the policy level in terms of nutritional guidance.

Nutrition

Food Trends ’26: Higher Standards

The Dirt

This year's food trends reflect the realities of financial pressures, smaller appetites, and information fatigue, while still wanting food to support health, comfort, and functionality. This shift is showing up not only in consumer behavior, but increasingly in how nutrition itself is being discussed at the policy level in terms of nutritional guidance.

I love writing this piece every year, partly to see what’s coming, and partly to sanity-check what I’m already noticing in real life: smaller meals, tighter budgets, and way less patience for complicated food advice.

As Statista summarizes in its Consumer Trends 2026 reporting, consumers are more than ever, “increasingly deliberate about spending, prioritizing value and practicality over abundance.” Mintel echoes this framing, noting that food choices are becoming less aspirational and more rooted in everyday function. FoodNavigator’s 2026 outlook reinforces the same point, stating that the coming year is defined by “integration rather than disruption” across food and beverage categories.

When read together, these three trusted sources for consumer insights and market outlook, all point to the same conclusion: consumers are simplifying how they eat while also raising expectations for what their food delivers. The result is a move away from rigid food rules and toward food choices that combine multiple nutritional benefits and practical value.

This is not a rejection of recent food trends. It is an evolution shaped by economic constraints, new medical realities, and a more mature understanding of nutrition. In other words: the era of ‘food as identity’ is cooling off. ‘Food as a set of tools in a toolbox’ is heating up.

1. The Context: Constraint, Caution, and Choice Fatigue

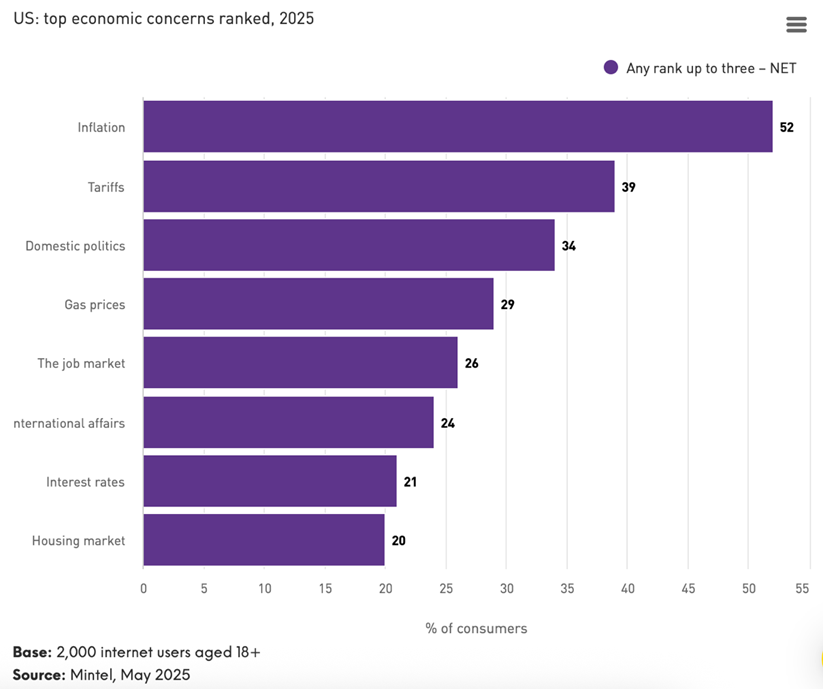

Eating well gets harder when life is expensive and decision-fatigue is real. Statista’s Consumer Trends 2026 finds households across major global markets remain financially cautious: inflation, tariffs, and cost-of-living pressures are still shaping spending, even alongside cautious optimism.

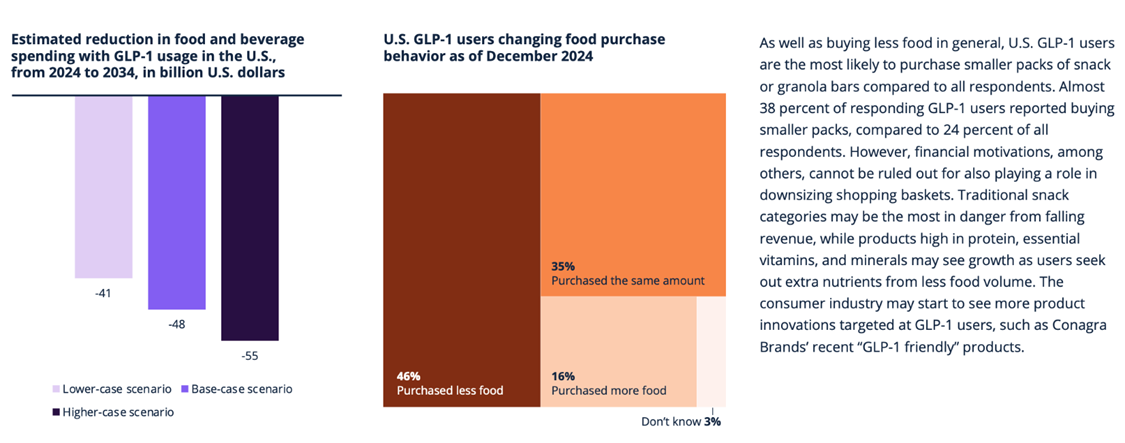

Food sits in a unique place in this landscape. Consumers may cut back on discretionary categories, but food trade-offs feel personal. Statista suggests 60%+ of consumers are actively looking for better value in food purchases, not simply buying less. That shows up as fewer impulse buys, closer scrutiny of ingredient lists and health claims, and higher expectations that foods deliver more than one benefit—especially as people consolidate eating occasions (hello, GLP-1 era) and think more about longevity.

Mintel frames this as a shift away from “aspirational eating” and toward functional, reality-based eating that supports long-term health. FoodNavigator similarly notes growing intolerance for complexity and exaggerated claims—particularly when products promise transformational outcomes that don’t match everyday use.

As FoodNavigator puts it:

“The longevity trend is relevant to almost everyone. Consumers wanting to ensure they live a longer, better quality life, are being encouraged to start paying attention to their health at a much younger age.”

Examples of this growing skepticism are increasingly evident across the food landscape. Consumers are questioning products marketed as “detoxifying,” “hormone-balancing,” or “metabolism-resetting” when those claims aren’t backed by clear, substantiated benefits. There’s also rising frustration with foods positioned as meal replacements that still require add-ins, supplements, or prep to be “complete.”

Ingredient lists and front-of-packaging claims filled with buzzwords, natural, grass-fed, adaptogens, nootropics, superfoods, are losing credibility when brands can’t explain what they do or why they matter. Highly restrictive “perfect” diet frameworks are facing similar pushback when they assume ideal schedules, unlimited budgets, or unrealistic cooking habits. (And honestly? It’s about time.)

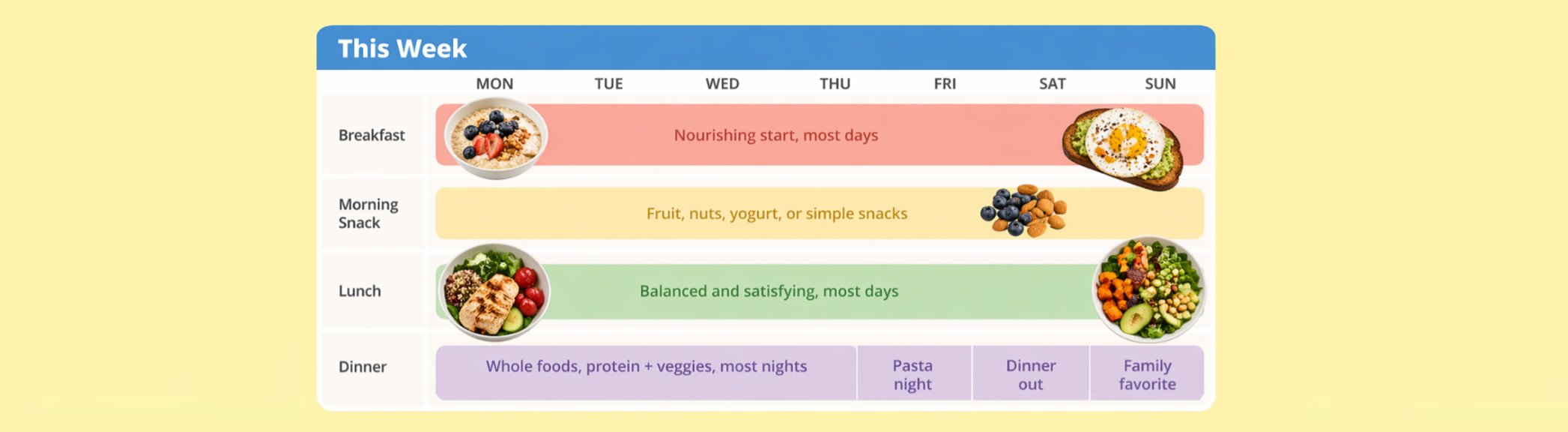

In contrast, foods that clearly communicate what they do—delivering satiety, convenience, or basic nutrition—are gaining trust as consumers prioritize simplicity and practicality. Think: high-protein staples like Greek yogurt, cottage cheese, eggs, and rotisserie chicken; no-prep snacks like nuts, jerky, hummus, and cheese sticks; and predictable convenience foods like bagged salad kits, microwaveable grains, and frozen meals that plainly list calories and protein.

These are the “no drama” foods—the ones that actually get eaten on busy weekdays. Even functional categories earn more credibility when the purpose is straightforward, like electrolytes for hydration or fiber-forward basics like oats and beans, rather than dressed up as a transformation.

This shift away from aspirational eating and toward functional, everyday nutrition is now being echoed beyond the marketplace. In January 2026, the U.S. Department of Agriculture announced a significant reset in U.S. nutrition policy, explicitly emphasizing a return to real food, protein, fruits and vegetables on the TOP of the food pyramid as the foundation of health.

The message reflects growing recognition that increasingly complex guidance, layered claims, and rigid dietary frameworks have not translated into better health outcomes such as reduced cancer, heart disease, diabetes, and Alzheimer’s.

“American households must prioritize whole, nutrient-dense foods—protein, dairy, vegetables, fruits, healthy fats, and whole grains—and dramatically reduce highly processed foods. This is how we Make America Healthy Again.”

-U.S. Food & Drug Administration

Together, consumer behavior and policy direction point to the same conclusion: nutrition strategies that resonate in 2026 are those that emphasize efficiency, nutrient density, and practicality, not optimization for its own sake.

2. From “Maxxing” to Nutrient Density

For much of the past decade, food trends have had a strong emphasis on singular nutritional goals: high protein, low carb, plant-only. While these approaches brought attention to important nutrients, they also encouraged narrow thinking, something we know can cause nutrient imbalances and generally poor nutrition.

Statista data shows that the rapid adoption of GLP-1 medications is accelerating a shift away from eating for quantity alone. GLP-1 users consume about 30% fewer calories on average, are choosing smaller portions, and increasingly look for foods that deliver satisfaction and nutrition without excess. As Statista analysts note, consumers impacted by appetite-suppressing medications are “reframing health around efficiency rather than quantity,” i.e.- what gives you the most nutrients in the least amount of calories.

As a result, protein is no longer disappearing, but it is changing form.

What consumers are moving away from:

- Protein bars and shakes engineered almost entirely around protein grams

- Products positioned as nutritionally sufficient based on a single claim.

What is gaining relevance:

- Naturally protein-rich foods with added nutritional benefits, such as skyr-style yogurts from brands like Siggi’s or Icelandic Provisions, which deliver high protein alongside calcium and live cultures, or lentil-based pastas like Barilla Red Lentil, which provide protein, fiber, and iron in a familiar format.

- Strained and fermented dairy formats, including Two Good Greek Yogurt or Chobani Complete, which pair protein density with probiotic support and bone-health nutrients such as calcium and vitamin D.

- Balanced, mixed meals built around whole ingredients—such as Amy’s Kitchen lentil bowls, Daily Harvest grain-and-legume blends, or Sweetgreen warm bowls—that deliver protein as part of a broader matrix of fiber, complex carbohydrates, and micronutrients rather than as an isolated add-on.

Mintel characterizes this transition as a move away from “nutrient maxxing” toward what it calls “nutritional efficiency,” where foods are expected to deliver multiple benefits within smaller portions. FoodNavigator similarly notes growing skepticism toward one-note nutritional messaging, observing that “consumers are no longer impressed by single claims divorced from real eating habits.”

3. Fiber Becomes Foundational

Fiber has long been recommended but rarely prioritized. In 2026, it is predicted to become critical rather than supplemental.

Statista highlights that younger consumers, particularly Gen Z, are increasingly motivated by long-term health and prevention, while still constrained by cost, time, and overwhelm. Fiber uniquely addresses these pressures by supporting gut health, blood sugar regulation, and satiety without requiring radical dietary change. As Statista notes, preventative health is increasingly pursued through “everyday food choices rather than specialized interventions.”

Rather than adding fiber as a standalone supplement, many brands are embedding it directly into familiar, everyday foods. This is showing up in fermented plant-based yogurts such as Cocojune, which pair live cultures with naturally fiber-containing ingredients, as well as in breads made with whole grains and seeds that deliver four to six grams of fiber per slice, including Dave’s Killer Bread varieties. Fiber-forward snacks are also gaining traction, with products like Biena roasted chickpeas and Nature Valley oat-based bars offering naturally occurring fiber in formats consumers already recognize and trust.

FoodNavigator reports that fiber is increasingly positioned as a partner to protein, stating that brands are using fiber to help foods feel “more complete and more satisfying in a lower-calorie context.”

4. Traditional and Shelf-Stable Foods Are Reframed

Economic pressure is reshaping how consumers define quality and value. Statista notes that while consumers still allow small indulgences in food, those indulgences must feel reliable and worth the cost. As one Statista insight summarizes, consumers are “trading down selectively but trading up emotionally.” Prioritizing familiarity over complexity.

As a result, shelf-stable and traditional foods are being re-evaluated, not as lower-quality compromises, but as strategic, practical choices in a constrained food environment. Consumers are rediscovering formats that balance nutrition, affordability, and reliability. Canned beans and lentils, which provide affordable sources of protein and fiber with long shelf lives and minimal preparation are gaining in popularity. Frozen vegetables, which retain nutritional value while reducing food waste and saving time in everyday cooking are becoming more desirable.

FoodNavigator’s 2026 trend analysis highlights renewed interest in traditional formats across dairy and pantry categories, as consumers gravitate back toward foods that feel practical in uncertain times. This includes staples such as milk, yogurt, cheese, canned beans, lentils, soups, and frozen vegetables, formats that are familiar, versatile, and easy to store or prepare. The emphasis is not nostalgia, but reliability: foods that consistently deliver nutrition, value, and ease without requiring consumers to adopt new habits.

5. Technology as a Tool for Continuity

The long-standing natural-versus-processed debate is giving way to pragmatism. Statista’s consumer research shows openness to food technology when benefits are clear, transparent, and tied to real-world challenges such as cost, waste, or environmental pressure.

Mintel notes that consumers are increasingly comfortable with food technology when it is framed as supporting existing food systems rather than reinventing them. Acceptance is highest when innovation preserves familiar taste, texture, and usage, while quietly improving environmental or nutritional performance behind the scenes.

In practice, this is showing up through technologies that enhance foods people already recognize:

Precision fermentation, for example, is being used to produce dairy-identical proteins that perform just like traditional whey and casein in familiar products. Companies such as Perfect Day supply fermentation-derived dairy proteins that are used in ice creams, yogurts, and beverages that look, taste, and behave like their conventional counterparts, but with significantly reduced land and water use. This allows brands like Straus Family Creamery and plant-forward innovators to create products with the sensory qualities consumers expect while lowering environmental impact.

Upcycling dairy byproducts is another area gaining traction. Brands like Wheyhey! repurpose whey proteins into high-quality nutrition bars and protein snacks, turning what was once a low-value stream into a consumer-ready ingredient. Similarly, companies such as Renewal Mill incorporate upcycled whey into baking mixes and snack products, reducing waste while enhancing protein content and delivering the texture and flavor that customers recognize from traditional bakery items.

FoodNavigator reinforces this framing, observing that innovation is most successful when it is “used to protect familiar foods, not ask consumers to abandon them.”

“Let food be thy medicine and medicine be thy food.”

– Hippocrates

What This Means for 2026

Taken together, the data tells a coherent story: consumers are seeking foods that fit their lives, financially, nutritionally, and emotionally.

This is not a vilification of 2025 trends. It is an evolution driven by greater knowledge and tighter constraints. As appetites shrink and expectations rise, food choices become more integrated and more realistic.

The Bottom Line

The defining food trend of 2026 is balance under pressure. Brands that succeed will be those that respect consumer limits, deliver multiple benefits per bite, and communicate with clarity rather than hype.

Share this article

Listen to the Dirt to Dinner Podcast